Please welcome my guest blogger, Barbara Stapleton, who teaches middle school students about personal finance. Today, she is going to be sharing her lessons on how to teach tweens about credit cards versus debit cards because this is not the kind of personal finance lesson you want your kids to learn the hard way!

p.s. I have another related post: Top 10 Life Skills Kids Need Before College.

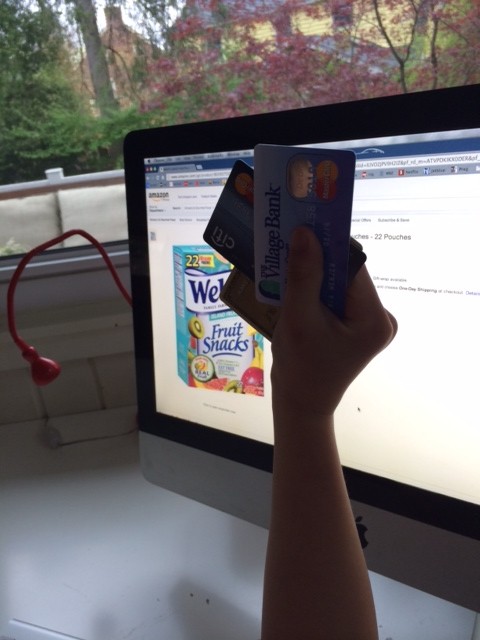

Credit and Debit cards Personal Finance for Kids

Figuring out how the world works beyond junior high school can be daunting. Students feel like they are grown and need and crave autonomy in their lives, but over and over again, students find there are still so many things they don’t have a solid understanding about and one of the big things is credit cards (and debit cards). Even though they aren’t yet the age where they can apply and use a credit/debit card, they still need to have the foundational understanding of credit cards BEFORE they begin using them. As many of us have learned over the years, learning as you go in financial education can be devastating!

I’ve been teaching programs over six weeks at local junior/middle high schools that cover several topics, including self-knowledge and career selection, goals for their financial future, budgeting and keeping balance, understanding credit scores, and learning the financial effects of risk. But by far, the critical content that I find students don’t think about or have skills in credit and debit card use and how to be skilled at spending so they are successful in managing money. (It’s from Junior Achievement, there I said it, but I promise I just volunteer to teach, I don’t work for ‘em! You have to give credit for the curriculum where credit is due!)

Although it may sound dry to us, students get very involved in the discussion when they see that how they use or misuse a credit/debit card can affect any future spending they may want to do. Because we all enjoy spending!

Here are the key points of our class:

Debit cards 101 for Kids

Buy Now; Pay Now

- The money that you access on a debit card comes from your checking or savings account, so you pay for it immediately.

- There are not any interest charges on debit card purchases.

- If you don’t keep track of your account balance, overdrafts may happen.

- Debit cards are a good choice for everyday purchases, particularly what I like to call consumable purchases (consumable – anything that doesn’t last for a reasonable amount of time – food at restaurants, groceries, gasoline, you get the picture)

- BE AWARE: debit card holders can be held accountable for up to $500 of unauthorized purchases if the card isn’t reported as stolen within 48 hours, so this is why it’s important to track your spending and know what’s going on in your account (but that’s another lesson).

Credit cards 101 for Kids

Buy Now; Pay Later

- Credit cards are NOT tied to a checking or savings account. Credit cards at the most basic understanding are a loan.

- Going to say it again money available on credit cards is pre-approved credit. It is borrowed (a loan) from the bank and paid back later.

- There is an interest rate charged on unpaid monthly credit card balances. That interest rate (APR) carries over from one month to the next on any of those unpaid balances.

- Interest rates vary. Interest rates can vary, A LOT. Yes, you may get an introductory 0% interest rate, but it’s only introductory and if you don’t get all that you charged up paid off before the introductory period over, then guess what – you’re paying interest on what’s left. So all those sale items aren’t so much on sale anymore!

- Those rates depend on a lot of things know as ‘creditworthiness’, which is just basically – how much you owe (debt), how much you make (income), your credit score, and if you’ve been paying ALL of your payments and bills on time.

- There are limits on the credit card ‘loan’ you have, you can’t just spend and spend. Remember, they know how much you make and how much you owe to others, so they have to put a limit on the credit card.

- You get a monthly statement (might be in the mail, or you could have them send it to your e-mail or get it through a log-in account on their website). You have to have some money from a job or other income to pay that balance every month.

- The best thing about credit cards – they’re great for emergencies. They’re also good for protecting you when you make online purchases. Why? If your card or the number is stolen, you should only be responsible for the first $50 of unauthorized charges. That’s a relief!

Credit or Debit?

There are benefits to both cards. The ability to understand what those benefits are and the reasons to use one over the other is the foundation of our class discussions. Once students know why they should use a debit card instead of a credit card to buy a disposable/consumable item (groceries, haircuts, pet food) and how a credit card can help establish credit and the credit score (that we talk about in another class session), they have skills to be successful in managing their financial future.

The great thing about the credit/debit card lesson (and the others, too) are fun ‘games’ that the students play to really get the information across. There’s a whole challenge game where they are timed and ‘quizzed’ to decide which activity should use or is a trait of credit or debit card. They get it! They improve with every ‘round’ and they support their classmates in explaining and understanding answers.

And once we’ve completed a lesson, we view a 1 minute video, it’s not part of the rest of the curriculum, but I’ve found it’s essential in giving them something that they can view when they aren’t in the classroom. It drives home in presentations and classes to repeat and repeat viewing and listening to anything on financial literacy because it takes a while to all sink in. These videos completely help with the repetition component, because there are over 200 videos to view on their own time, at their own pace. The one we use for the credit card class is found at Professor Savings here because it not only mentions credit card use, but it also gives good general tips to reinforce the spending habits we’ve talked about in class.

For over ten years, I provided student loan, money management, and financial literacy training on university and college campuses to both undergraduate and graduate students, from technical programs to professional programs. The one thing I almost always came away with after a training session was that we weren’t educating these students soon enough and that college (and high school) wasn’t when we needed to start. It begins at home, but we know that’s not always where it can or will happen, because parents or guardians may never have had the financial literacy skills taught to them either. Offering the skills during middle/junior high school, and then continuing to reinforce them throughout each school year afterward is critical to moving forward and finding true financial education for our next generation. It’s never too early to start learning financial literacy.

Barbara Stapleton is currently an associate director for career and technical education for the Kansas Board of Regents. She has 14 years of higher education experience and over 16 years of marketing, sales, and professional development experience. Before joining KBOR, Barbara worked as the senior regional account executive for Texas Guaranteed Student Loan Corporation in the Rocky Mountain Region and provided professional development training for educators and administrators as well as financial literacy training for trainers and students at educational institutions throughout the region. She holds a bachelor’s in political science from Purdue University and a master’s in management from Baker University.

p.s. Related posts:

Teaching Kids About Money: Summer Curriculum

Who Owns the Money? Economics for 4th Graders

How To Teach Kids About Money Management

Teaching Kids about Money: Spend, Save, Donate

Top 10: Ways to Teach Kids about Money

Teaching Kids About Money TWITTER PARTY

Money Lessons: 5 Key Ways to Teach Your Kids About Money

8 Tips for Teaching Your Kids Financial Responsibility

5 Simple Tips to Manage Your Money as a Parent

Follow PragmaticMom’s board Life Skills for Kids on Pinterest.

My books:

BEST #OWNVOICES CHILDREN’S BOOKS: My Favorite Diversity Books for Kids Ages 1-12 is a book that I created to highlight books written by authors who share the same marginalized identity as the characters in their books.

This is one of the best programs that I have seen for children and finances. I hope that lots of schools will adopt it.

Hi Barbara,

Thanks so much! I’ve read that a lot of schools are starting to incorporate Personal Finance into the curriculum; mine school hasn’t yet so I will do it at home and these type of programs might work for that too.

Totally agree. I wish all middle schools offer programs like this. I volunteered for Junior Achievement and really liked their curriculum.

Hi iGameMom,

I think that some schools are offering personal finance in high school but it would be great to have this in middle school too. Mine middle school isn’t doing it though, at least, that I know of.

I’d love to hear more about the Junior Achievement curriculum. That’s new to me.

I love JA! I volunteered at my son’s school for JA this year. I was terrified (that was WAY outside of my comfort zone) but it was actually fun. They have it down to a science and my son always loves it. Next year, I think they start going TO the local JA office. (FYI, I did not volunteer in my son’s class – he didn’t want me to!)

Hi Dee,

The JA program sounds great! I don’t think we have that here or at least it’s new to me! What is TO? Sounds like a great experience for the kids AND volunteers!!

Great points! 😀 This will really help me when I get older! 🙂

Thanks Erik! I’ll bet you will be able to teach a class on personal finance for kids when you are older! 🙂

This is SO important for kids to learn! Great post.

Hi MaryAnne,

I’m so glad Barbara wrote this for me! My kids need to learn this too!

I think this is a topic that is all too often skipped by many schools. Kudos to you for showcasing it and to Barbara for teaching it! I wish more skills focused on life skills like this as much as test scores.

Hi April,

That’s a good point. Life lesson skills like credit card debt should be taught in schools. I’m reading articles that many high schools are starting to add this but I haven’t heard of many middle schools (yet).

Great article! I’m very interested in the game you mentioned. I’m looking for a game to play with the kids in our 4-H club in order to teach them about credit & debit. I looked on the JA website but can’t find the curriculum you are using. Also, is it something I would be able to access? Do they sell it? Thanks for your help.

Hi Sweettater,

I have some free personal finance games for kids here: http://www.pragmaticmom.com/helpful-links/personal-finance-kids/

Hope this helps!